As a foreigner working in China, understanding the income tax system is essential to ensure compliance with local regulations and avoid any potential penalties. Here's an overview of income tax for foreigners working in China:

1. Tax Residency:

Tax residency in China is determined based on the number of days an individual spends in the country within a tax year. Generally, individuals who reside in China for 183 days or more in a tax year are considered tax residents and are subject to Chinese taxation on their worldwide income. Non-residents are only taxed on income derived from sources within China.

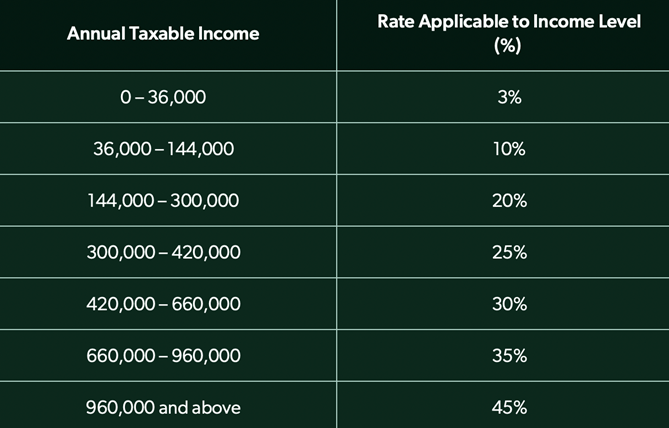

2. Tax Rates and Thresholds:

China's individual income tax (IIT) system consists of progressive tax brackets, with tax rates ranging from 3% to 45%. The tax rates and income thresholds may vary depending on the individual's residency status, marital status, and other factors.

3. Taxable Income:

Taxable income for foreigners working in China includes salaries, wages, bonuses, allowances, and other forms of compensation received for services rendered within China. Certain deductions and allowances may be available to reduce taxable income, such as social insurance contributions, housing allowances, and education expenses for dependents.

4. Tax Treatment of Benefits and Allowances:

Benefits and allowances provided to expatriate employees, such as housing, transportation, and education allowances, may be subject to taxation in China. Employers are required to report and withhold taxes on these benefits in accordance with local regulations.

5. Tax Filing and Withholding:

Employers in China are responsible for withholding and remitting individual income tax on behalf of their employees through monthly payroll deductions. Employees are required to submit an annual tax reconciliation declaration to the tax authorities by the end of March following the tax year to reconcile any discrepancies and settle any outstanding tax liabilities.

6. Double Taxation Agreements (DTAs):

China has entered into double taxation agreements with many countries to prevent double taxation of income for individuals who are tax residents of both China and another country. These agreements typically provide mechanisms for determining tax residency, allocating taxing rights, and providing relief from double taxation through tax credits or exemptions.